TLDR: For 30 years, the PE playbook was simple: more capital, more leverage. That era is over. AI/ML deal value tripled from $41.7B to $140.5B in a single year. PE-backed companies with systematic AI capabilities have nearly 2x the ROIC of those without. The firms winning the next decade won’t just be using AI — they’ll be deploying autonomous agents across the entire deal lifecycle. Here’s the full playbook.

The Old Playbook Is Dead

There’s a number that should make every GP sit up straighter now.

AI and machine-learning deal value in private equity more than tripled in a single year — from $41.7 billion in 2023 to $140.5 billion in 2024. This is more than just a trend, but a very strong signal flare for growth. [1]

And it’s not just deal flow. BCG’s latest survey found that PE-backed companies that systematically build AI capabilities across their functions have nearly twice the return on invested capital as companies that don’t. [2] Digital initiatives alone deliver 15–20% ROI. When AI is layered on top of a solid digital foundation, total returns can reach 30–35%. [2] Yes, those numbers are real. In some of the conversations with PE-backed businesses, they’re all trying to figure out their AI gameplan that will generate consistent real results.

The math is no longer ambiguous. AI isn’t a nice-to-have. It’s the new source of alpha.

For 30 years, the PE playbook was elegant in its simplicity: find a good business, add leverage, cut costs, grow EBITDA, exit at a multiple. Financial engineering was the edge. Capital access was the moat.

That era is over. Or at least drastically changing.

Accenture’s 2026 outlook puts it plainly: PE’s operating model is being reframed — from leverage to learning speed, from balance-sheet engineering to operational precision, from scale of capital to depth of insight. [1]

The firms that figure this out first will compound their advantage every quarter. The ones that don’t will be paying a premium to acquire businesses that AI-native competitors already identified, diligenced, and closed on faster.

Why Most Firms Are Still Stuck

Here’s the uncomfortable truth: most PE firms, like most businesses, are still stuck in “AI pilot purgatory.”

They’ve bought the tools. They’ve run the pilots. They’ve hired a “Head of Digital” and put together a task force. And they’re getting marginal gains — maybe a few hours saved on LP reports, maybe a slightly faster first-pass screen on inbound deals.

The problem isn’t the technology. The problem is the mental model.

Most firms are asking the wrong question. They’re asking: “How can AI help us do what we already do, but faster?”

The leaders are asking a completely different question: “What becomes possible when we have an autonomous agent whose only job is to monitor every company in our target universe, 24/7, and surface the ones that match our thesis before anyone else sees them?”

That’s not an efficiency play. That’s an actual REAL structural advantage.

And the window to build it is closing. BCG found that more than 90% of investment professionals plan to expand portfolio-level digital budgets over the next three years. [2] The race is on. The question is whether you’re building the infrastructure now, or playing catch-up in 2027.

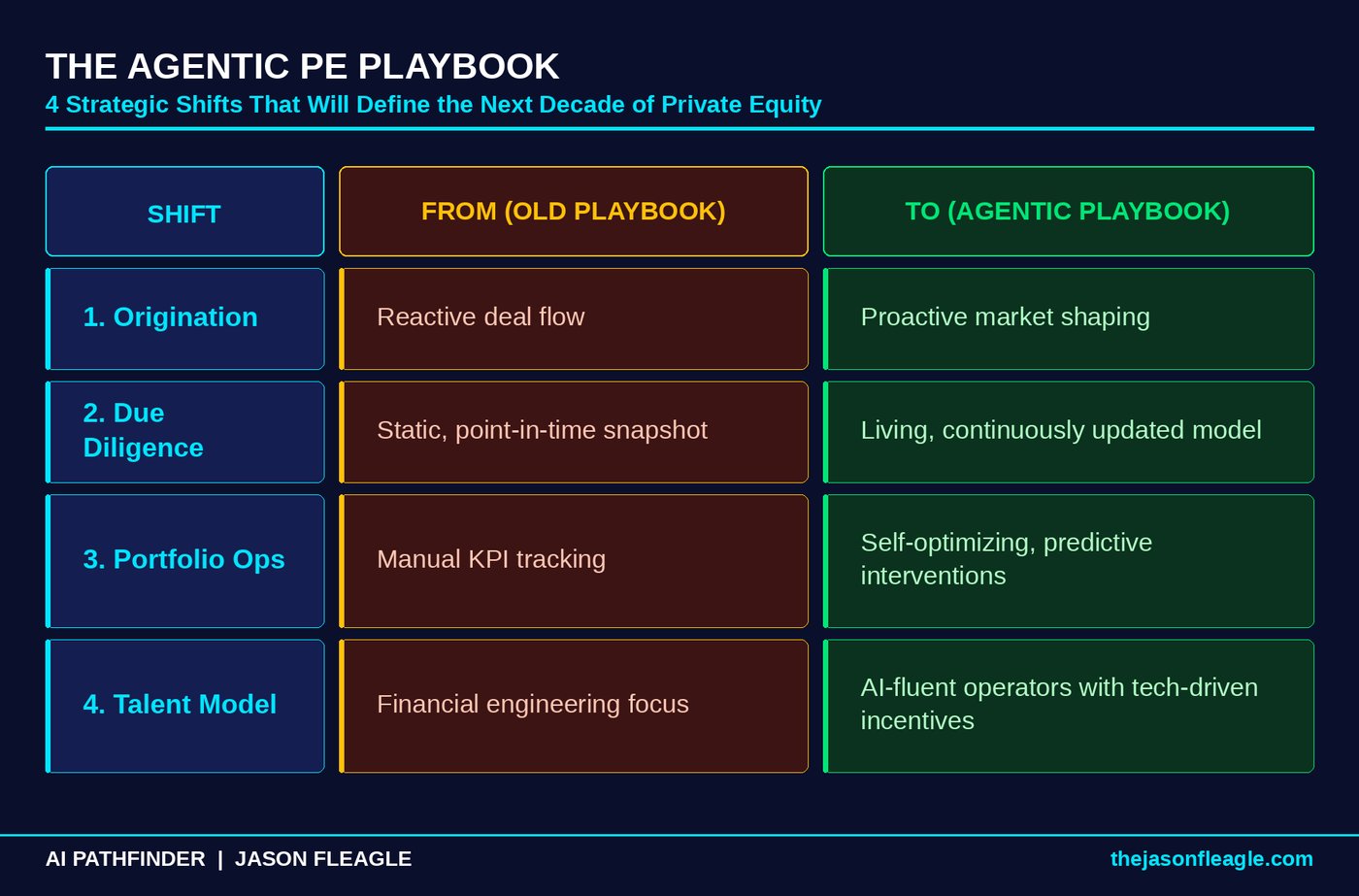

The Four Shifts That Define the Agentic Playbook

Accenture’s research outlines four domains where the transformation from AI-enabled to AI-native is already happening. [1] This is the new deal lifecycle:

Shift 1: Intelligent Origination. Agentic AI compresses the gap between signal and action. By autonomously scanning filings, sentiment, and sector chatter, AI surfaces hidden targets before the market reacts. This turns origination from a reactive process — waiting for bankers to send you deals — into proactive market shaping where your agents are already watching 10,000 companies and flagging the ones that match your thesis in real time.

Shift 2: Living Due Diligence. Diligence is evolving from a static snapshot to a living model. Agentic systems continuously ingest financial, operational, and ESG data, automate document review, and simulate synergy confidence ranges to drive faster, evidence-based investment decisions. The 90-day diligence sprint becomes a continuously updated model that your team can interrogate at any point in the process.

Shift 3: Self-Optimizing Portfolio Operations. Post-acquisition, AI agents monitor KPIs, learn from interventions, and recommend next-best actions — adjusting pricing, refining segmentation, optimizing working capital. This is the difference between a quarterly board review and a real-time operational intelligence layer that’s always on. Now with AI agents, the tools have never been easier to connect to the different platforms and tools that are already being used at the business.

Shift 4: Talent and Operating Model Transformation. AI-fluent operators are becoming indispensable. Incentives are shifting toward measurable value levers — pricing, productivity, and digital growth. In GP back offices, high-throughput workflows are automated, freeing teams to focus on insight generation and strategic intervention. The elite PE team of the future is small, senior, and directing armies of AI agents.

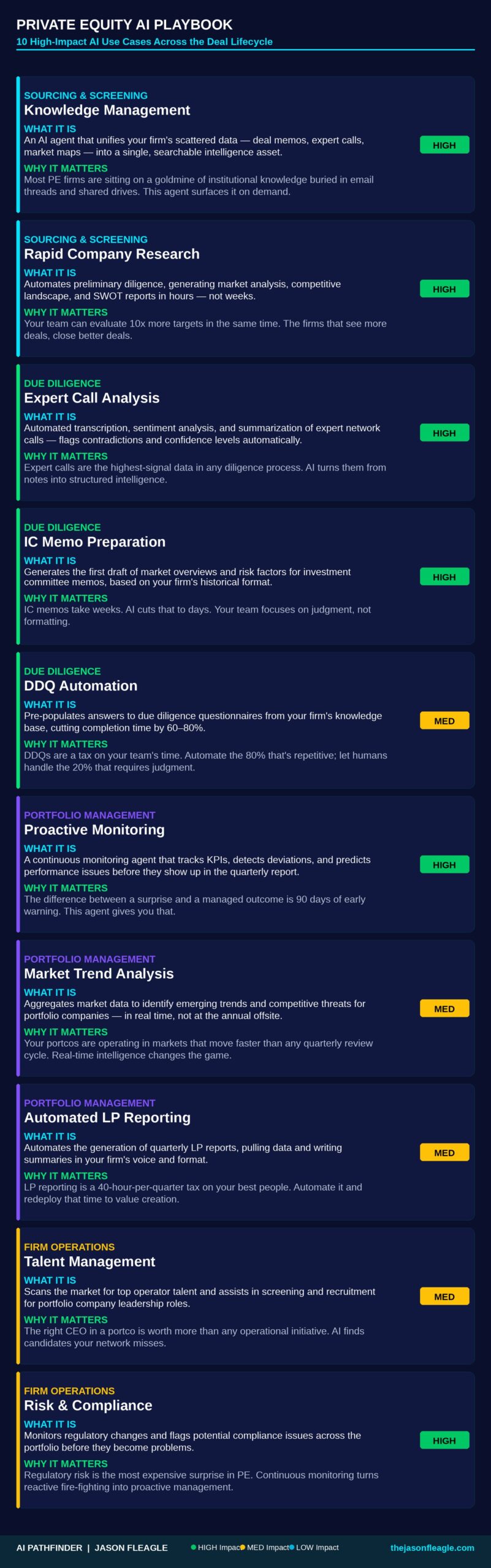

10 High-Impact AI Use Cases Across the Deal Lifecycle

I wanted to create some low-hanging fruit AI use cases that serve as a roadmap. Start with the area of your PE firm that has the most friction, and use that as your wedge to build momentum and internal expertise. [3]

The Great PE Divide Is Coming

I’ve been watching this space closely, and here’s what I see happening over the next 24 months.

There will be two types of PE firms.

The “Renters” will continue to treat AI as a productivity tool — a faster way to do the same work they’ve always done. They’ll subscribe to a few platforms, run some pilots, and declare victory when an analyst saves four hours a week on LP reports. They’ll be AI-enabled. They will not be AI-native.

The “Owners” will rebuild their operating model around intelligence as a core asset. They’ll deploy dedicated agents for origination, diligence, and portfolio monitoring. They’ll build proprietary data flywheels that get smarter with every deal. They’ll have a compounding advantage that gets harder to close every quarter — and they’ll exit at higher multiples because their portfolio companies will be demonstrably more AI-ready.

Which one sounds better to you?

BCG’s data makes the stakes clear: 40% of investors have already experienced a valuation haircut of 5% or more due to digital maturity gaps. [2] That number is going to climb as buyers get more sophisticated about assessing AI readiness. The firms that build now will command a premium at exit. The ones that don’t will be explaining the discount. AI-native companies are becoming a non-negotiable.

The window to build this infrastructure is open right now. It won’t be open forever.

Your 3-Step Action Plan

1. Diagnose Your Biggest Bottleneck First

Don’t start with the flashiest AI tool. Start with the most painful part of your process. Is your deal flow weak? Focus on Knowledge Management and Rapid Company Research. Is your diligence process a slog? Target Expert Call Analysis and IC Memo Prep. Are you constantly surprised by portfolio company performance? Build a Proactive Monitoring agent. Pick one, go deep, and measure the results before you scale. Think about the three areas of people, process, and technology and you’ll have a good idea of where to start. Or feel free to ask me or my team.

2. Pilot Your First Agent in Due Diligence

Diligence is the most data-intensive, time-sensitive part of the deal process — and the highest-leverage place to start. Begin with Expert Call Analysis or DDQ Automation. Both have clear inputs, measurable outputs, and immediate time savings that build internal credibility for the broader AI transformation. Set a 60-day pilot with a defined success metric: hours saved, accuracy improvement, or analyst capacity freed up.

3. Build Toward a Proprietary Data Flywheel

The firms that win long-term won’t just be using AI tools. They’ll be building proprietary intelligence assets — deal databases, sector models, and portfolio benchmarks that get smarter with every transaction. Every deal you run through an AI-assisted process generates data. Start capturing it now. The compounding effect of a well-structured data flywheel is the most durable competitive advantage in the agentic era. If you need help structuring this, reach out to our team.

Ready to Build Your AI Strategy?

If you’re a PE firm, portfolio company, or business leader trying to figure out where to start with AI, here’s how we can help:

- 🔹 Work with Jason 1:1 — AI strategy, agent deployment, and implementation

- 🔹 Read the Case Studies — Real-world AI implementations with measurable ROI

- 🔹 Subscribe on YouTube — Weekly breakdowns of AI tools, strategies, and deployments

- 🔹 The AI Marketing Course — Learn to build AI-powered marketing systems that generate revenue

About Jason Fleagle

Jason Fleagle is a Chief AI Officer, AI architect, and founder of Catalyst Brand Group — an AI consulting agency focused on revenue-first, real-world AI deployments. He has helped businesses generate over $70M+ in revenue through AI strategy, automation, and agentic systems. His work focuses on practical, ROI-driven AI implementations that deliver measurable results in time savings, cost reduction, and workforce transformation.

References

- Accenture — Agentic AI Is Redefining Private Equity — https://www.accenture.com/us-en/blogs/strategy/ai-redefining-private-equity

- BCG — Private Equity’s Future: Digital-First and AI-Powered — https://www.bcg.com/publications/2026/private-equitys-future-digital-first-and-ai-powered

- Blueflame AI — AI Use Cases for Private Equity — https://www.blueflame.ai/resources/ai-use-cases-for-private-equity