AI Pathfinder | Issue #54 | April 28, 2026 | By Jason Fleagle

Microsoft ends the Azure-only era with OpenAI’s AI Models. China forces Meta to unwind its $2B Manus acquisition. Two deals. One unmistakable signal: the rules of enterprise AI just changed.

Two headlines dropped this week that fundamentally rewrite the rules of the enterprise AI market. The “Wild West” era of exclusive cloud deals and borderless AI acquisitions is over. We are entering the era of Strategic Sovereignty — a world where AI infrastructure is shaped as much by geopolitics and financial engineering as it is by model benchmarks.

First, Microsoft and OpenAI amended their $13 billion partnership, ending the “Azure-only” era and allowing OpenAI to serve its models directly on AWS and Google Cloud. Second, the Chinese government ordered Meta to unwind its $2 billion-plus acquisition of agentic AI startup Manus on national security grounds, giving both companies a preliminary deadline of several weeks to fully reverse the transaction.

These are not incremental updates. They are structural shifts in how AI infrastructure is bought, sold, governed, and — increasingly — weaponized as a strategic national asset. Here is what every AI operator needs to understand before the week is out.

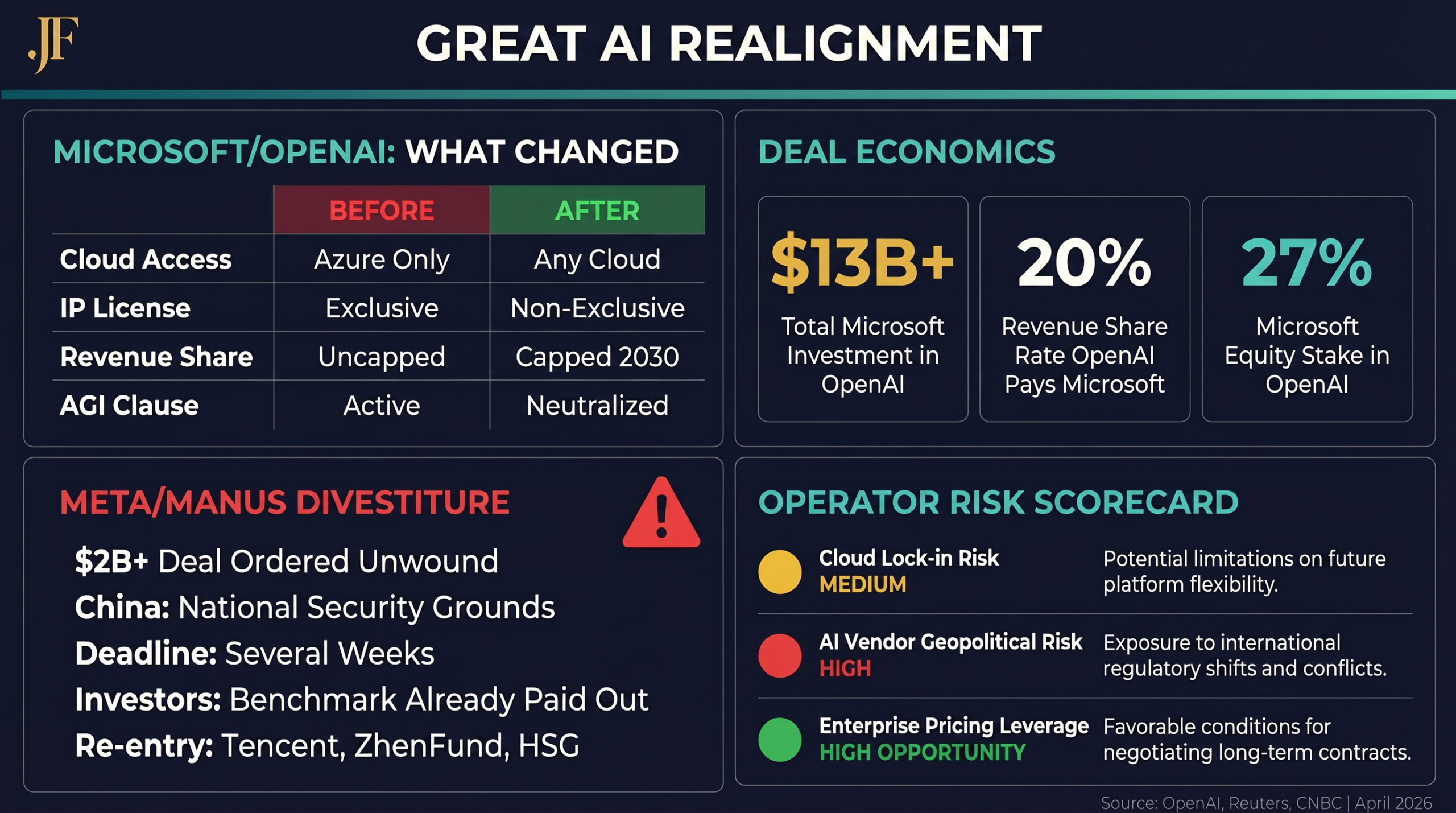

Feature 1: The Microsoft/OpenAI Decoupling — The End of Azure-Only

For years, the rule was simple: if you wanted OpenAI’s frontier models in your enterprise stack, you went through Microsoft Azure. That exclusivity was the cornerstone of Microsoft’s AI strategy and the foundation of a $13 billion investment relationship that began in 2019. Today, that wall has come down.

On April 27, 2026, the two companies published a joint announcement confirming an amended agreement grounded in what they called “flexibility, certainty, and a focus on delivering the benefits of AI broadly.” The language is diplomatic. The implications are seismic.

The Deal Breakdown: Old vs. New

| Term | Old Agreement | New Agreement (April 2026) |

|---|---|---|

| Cloud Exclusivity | OpenAI products exclusive to Azure. No other cloud provider had direct access. | OpenAI can now serve all products to customers across any cloud provider (AWS, GCP, and others). |

| IP Licensing | Microsoft holds an exclusive commercial license to OpenAI models and products. | Microsoft holds a non-exclusive license through 2032. OpenAI can license its technology to other companies. |

| Revenue Share — Microsoft to OpenAI | Microsoft paid a revenue share to OpenAI when customers accessed models via Azure. | Microsoft no longer pays a revenue share to OpenAI. |

| Revenue Share — OpenAI to Microsoft | OpenAI pays 20% of revenue to Microsoft. No cap. | OpenAI continues paying 20% through 2030, but now subject to a total cap. |

| AGI Clause | Microsoft’s license could be revoked if OpenAI achieved AGI. | Effectively neutralized. Revenue share continues “independent of technology progress.” |

| Microsoft Equity | ~27% stake valued at $135B (October 2025 recapitalization). | Microsoft remains a major shareholder, participating directly in OpenAI’s growth. |

Why OpenAI Pushed for This

The driving force behind this amendment was OpenAI’s commercial ambition. OpenAI Revenue Chief Denise Dresser stated bluntly in an internal memo earlier this month that the previous exclusivity arrangement had “limited our ability to meet enterprises where they are.” That is a polished way of saying: we were losing deals because enterprise customers on AWS or Google Cloud refused to stand up a shadow Azure instance just to access GPT-5.5.

The scale of OpenAI’s cloud ambitions makes the constraint even more obvious. The company has committed to spending $250 billion on Microsoft Azure cloud services. It has also struck a $50 billion strategic partnership with Amazon, with AWS agreeing to invest up to $50 billion in OpenAI and serve as the exclusive third-party cloud distribution provider for OpenAI’s enterprise platform, Frontier. You cannot execute on $300 billion in cloud commitments through a single provider. The math demanded this change.

Why Microsoft Agreed

On the surface, giving up exclusivity looks like a concession. In practice, it is a masterclass in financial engineering. Satya Nadella traded a constraint that was increasingly unenforceable for three durable advantages: a guaranteed 20% revenue share (capped but certain through 2030), a non-exclusive IP license through 2032 that is explicitly “independent of technology progress,” and a 27% equity stake in a company whose valuation has only moved in one direction.

The elimination of the AGI clause is particularly significant for Microsoft’s enterprise customers. Previously, if OpenAI declared it had achieved Artificial General Intelligence, Microsoft’s license to the underlying technology could theoretically be revoked. That existential uncertainty is now gone. Microsoft can sell Azure OpenAI services to Fortune 500 companies with a clear runway to 2032 and no asterisks.

What Changes for Enterprise Operators

Amazon CEO Andy Jassy confirmed on X that AWS Bedrock will provide native access to OpenAI models within the coming weeks. Google Cloud’s Vertex AI integration is expected to follow. This means that for the first time, an enterprise running entirely on AWS or GCP can access GPT-5.5 natively — without a separate Azure subscription, without a separate billing relationship, and without the architectural complexity of a multi-cloud setup driven purely by model access.

The competitive pressure this creates on Azure pricing is real. Microsoft’s non-exclusive license means other cloud providers can now negotiate direct licensing deals with OpenAI. Enterprise buyers who have been locked into Azure OpenAI Service pricing should treat this as a renegotiation trigger. For more on the GPT-5.5 model itself, see our full breakdown of GPT-5.5 capabilities and benchmarks.

Feature 2: The Meta/Manus Divestiture — The Geopolitical Firewall

While OpenAI is tearing down cloud walls, a different kind of wall is going up. On April 27, 2026, the Wall Street Journal and Reuters reported that China’s commerce ministry has ordered Meta to unwind its $2 billion-plus acquisition of Manus, the Singapore-based agentic AI startup, on national security grounds.

This is not a regulatory delay or a request for additional disclosures. This is a forced divestiture. Beijing has given Meta and Manus a preliminary deadline of several weeks to fully reverse the transaction, restore Manus’s Chinese assets to their original state, and remove any data or technology previously transferred from Meta. Chinese regulators have also considered imposing penalties on both companies if the deal cannot be fully rescinded.

Why China Blocked It

The acquisition was completed in early 2026, and China’s commerce ministry announced an investigation just days after the deal closed. The stated rationale is national security — specifically, Beijing’s tightening scrutiny of U.S. investment in domestic startups developing “frontier technologies.” In practice, this means AI agents.

Manus is not just another chatbot company. It is one of the most capable autonomous AI agent platforms in the world, capable of executing multi-step tasks across web browsers, code editors, and enterprise systems without human intervention. From Beijing’s perspective, allowing a U.S. tech giant to own and control that technology — and the data pipelines it touches — is a strategic risk that outweighs any economic benefit from the acquisition.

The timing is also notable. The forced divestiture comes weeks before a planned mid-May summit in Beijing between U.S. President Donald Trump and Chinese President Xi Jinping. Whether the timing is coincidental or a calculated negotiating chip is an open question.

What Happens to Manus Now

The startup’s VC investors, including Benchmark, have reportedly already received their returns as part of the acquisition. Former Asian investors including Tencent, HSG, and ZhenFund are preparing to cooperate with the unwind and potentially re-enter as shareholders if the deal is reversed.

The practical outcome is that Manus reverts to a Chinese-majority-owned, Singapore-domiciled AI startup — operating in a geopolitical no-man’s-land that will make future U.S. enterprise deals significantly more complicated. Any enterprise that was planning to build critical workflows on Manus’s agentic platform should treat this as a vendor stability risk event.

The Broader Signal: AI Agents Are National Assets

The Meta/Manus divestiture is not an isolated incident. It is the clearest signal yet that AI agents — systems capable of autonomous action across digital infrastructure — are now classified as strategic national assets by at least one major global power. The implications for cross-border AI M&A are profound. Any U.S. company acquiring an AI startup with significant Chinese operations, Chinese investors, or Chinese user data should now model a forced divestiture scenario into its deal risk framework.

This also raises a harder question for enterprise operators: if your agentic AI platform has cross-border ownership or data flows, what is your contingency plan if regulators on either side of the Pacific decide to pull the plug? For context on the broader open-source AI competitive landscape, see our full breakdown of DeepSeek V4 — the leading open-source alternative.

The Strategic Takeaway: Three Shifts That Define the New Playbook

Cloud Agnosticism is the new standard. The Microsoft/OpenAI amendment confirms that the era of single-cloud AI lock-in is ending. Enterprises that have built their AI architecture around a single cloud provider’s model access will need to redesign for portability. The winners will be organizations that treat model access as a commodity and compete on the quality of their data, workflows, and governance layers — not on which cloud they chose in 2023.

Geopolitics is now a primary risk factor for AI M&A. The Meta/Manus divestiture is a case study that every corporate development team and AI vendor risk committee needs to read. The question is no longer just “is this model good enough?” It is “where is this company incorporated, who are its investors, and what happens to our workflows if a government intervenes?” AI due diligence now requires a geopolitical risk layer that most enterprise procurement processes do not yet have.

“Open” is winning over “Exclusive.” Whether it is OpenAI going cloud-agnostic, DeepSeek releasing open weights, or Meta’s Llama models proliferating across every cloud, the direction of travel is clear. Closed, exclusive AI ecosystems are under pressure from every direction — commercial, regulatory, and competitive. Operators who build on open or portable foundations are accumulating strategic optionality. Those who double down on proprietary lock-in are accumulating technical debt.

Your 3-Step Operator Action Plan

- Audit your cloud lock-in — and prepare to consolidate. If your organization is running a separate Azure subscription solely for OpenAI model access, you now have a clear path to consolidation. Map out your current Azure OpenAI usage, identify which workloads can migrate to Bedrock or Vertex once native OpenAI access is live, and build a 90-day migration plan.

- Stress-test your AI vendor’s geopolitical exposure. For every critical AI vendor in your stack, answer three questions: Where are they incorporated? Who are their major investors? Do they have significant operations, data flows, or user bases in China or other high-risk jurisdictions? Ensure your most critical AI workflows have a fallback — whether that is an open-weights model like DeepSeek V4 or Llama 3 that you can self-host, or a contractual right to export your data and workflows within 30 days.

- Renegotiate your enterprise AI agreements — now. Microsoft’s IP license to OpenAI is now non-exclusive. AWS and Google Cloud will soon offer direct OpenAI model access. This is the most favorable negotiating environment for enterprise AI buyers in three years. Do not auto-renew your Azure OpenAI Service commitments without running a competitive RFP.

Frequently Asked Questions

Does the Microsoft/OpenAI amendment mean I should move off Azure?

Not necessarily. If Azure is already your primary cloud and you are happy with the pricing and performance, there is no urgent reason to migrate. The amendment gives you optionality — the ability to access OpenAI models on AWS or GCP without a separate Azure relationship. Use that optionality as negotiating leverage on your next Azure renewal, even if you ultimately stay on Azure.

Is the 20% revenue share cap a significant number?

According to CNBC’s reporting, the 20% rate is unchanged — OpenAI continues to pay Microsoft 20% of revenue. What changed is that there is now a total cap on the cumulative amount. As OpenAI scales toward $10B+ in annual revenue, that cap becomes increasingly valuable to OpenAI’s bottom line and increasingly irrelevant to Microsoft, which has already secured its equity upside.

What does the Manus divestiture mean for users of the platform?

In the short term, Manus’s product and engineering teams are expected to remain intact. The divestiture is a corporate ownership change, not a shutdown. However, the uncertainty around future investment, product roadmap, and data governance makes it a high-risk dependency for enterprise workflows. Monitor the situation closely and avoid expanding your Manus footprint until ownership is clarified.

Could the same thing happen to other AI acquisitions?

Yes. Any U.S. company acquiring an AI startup with significant Chinese operations, Chinese investors, or Chinese user data should now model a forced divestiture scenario. The risk is not limited to China — the U.S. CFIUS process has also become more aggressive in reviewing inbound foreign investment in AI companies. Cross-border AI M&A is now a high-risk category on both sides of the Pacific.

What is the best fallback model if my primary AI vendor is blocked?

For most enterprise use cases, the strongest fallback options are DeepSeek V4-Pro (open weights, self-hostable, leading coding benchmarks) and Meta’s Llama 3.3 70B (widely available, strong general performance, MIT-licensed). Both can be deployed on your own infrastructure with no external API dependency. Building a “model router” that can switch between providers based on availability and cost is now a best practice, not a nice-to-have.

The Closing Question

In a world where cloud exclusivity is dead but geopolitical firewalls are rising, is your AI infrastructure built for flexibility — or are you still locked into the rules of 2023?

Drop your answer in the comments. I read every one.

Read the full article on LinkedIn: The Great AI Realignment: Cloud Independence and Geopolitical Firewalls

References

- OpenAI. (2026, April 27). The next phase of the Microsoft OpenAI partnership.

- Reuters. (2026, April 27). Meta prepares to undo Manus acquisition after China ban, WSJ reports.

- CNBC. (2026, April 27). OpenAI shakes up partnership with Microsoft, capping revenue share payments.

About Jason Fleagle

Jason Fleagle is the Chief AI Officer and founder of Catalyst Brand Group, an AI consulting agency specializing in revenue-first AI deployments, automation architecture, and enterprise AI strategy. He publishes the AI Pathfinder newsletter weekly for operators who want high-signal, decision-ready intelligence — not AI science projects.